How Long Does a Repossession Stay on Your Credit Report?

A repossession can have a significant impact on your credit score and overall financial health. Whether your car, furniture, or another financed asset is repossessed, this negative event will remain on your credit report for several years. Understanding how long repossessions stay on your credit report and how to recover is essential for rebuilding your credit.

What Is a Repossession?

A repossession occurs when a lender takes back property financed through a loan because you failed to make the agreed-upon payments. The lender has the legal right to reclaim the asset if you default on your loan, especially for secured loans like auto loans or furniture financing.

There are two main types of repossession:

- Voluntary Repossession

This happens when you willingly return the financed asset to the lender. - Involuntary Repossession

The lender reclaims the asset without your consent, typically after missed payments.

Both types negatively impact your credit score, though lenders might view voluntary repossession slightly more favorably.

How Long Does a Repossession Stay on Your Credit Report?

A repossession stays on your credit report for 7 years from the date of the first missed payment that led to the repossession. This period applies whether the repossession is voluntary or involuntary.

🚨 TUIC Errors + Low Credit Score?

CreditScoreIQ helps you build credit faster by reporting utility bills to all 3 bureaus—while you dispute errors.

Start Building Credit Today →- Start Date: The 7-year countdown begins from the date the loan first became delinquent (when you missed your payment).

- Impact: During this time, the repossession will appear under the “Negative Items” section of your credit report.

After 7 years, the repossession should automatically fall off your credit report. However, if it does not, you can file a dispute with the credit bureaus to have it removed.

How Does a Repossession Affect Your Credit?

A repossession can significantly lower your credit score and make it more difficult to obtain loans, credit cards, or favorable interest rates. Here’s how it impacts key aspects of your credit profile:

- Payment History (35% of your score):

Late or missed payments leading to repossession will damage your payment history, which is the most significant factor in determining your credit score. - Credit Utilization:

If the lender sells the repossessed asset for less than you owe, you may still have a deficiency balance. This balance can further hurt your credit if it’s sent to collections. - Creditworthiness:

A repossession signals to lenders that you’re a higher-risk borrower, making it harder to secure credit for years to come.

Impact of a Repossession on Your Credit Report

| Aspect Affected | Details |

| Credit Score Drop | Immediate and significant drop (50–150 points). |

| Duration on Credit Report | 7 years from the first missed payment. |

| Loan Eligibility | Reduced chances for loan approvals. |

| Interest Rates | Higher interest rates on future loans. |

| Credit Report Section | Appears under “Negative Items” or “Public Records.” |

Can a Repossession Be Removed Early?

In some cases, you may be able to remove a repossession from your credit report before the 7-year mark. Here are three methods to consider:

1. Dispute Errors on Your Credit Report

Check your credit report for errors, such as incorrect dates, payment details, or amounts. If you find inaccuracies, file a dispute with the credit bureaus (Experian, Equifax, and TransUnion) to have the error corrected or removed.

2. Negotiate a Settlement with the Lender

Contact your lender and ask for a “pay for delete” agreement. This involves paying off a portion of the deficiency balance in exchange for the lender requesting the repossession’s removal from your credit report.

3. Work with a Credit Repair Company

Professional credit repair services can help identify and address negative marks like repossessions, though results vary.

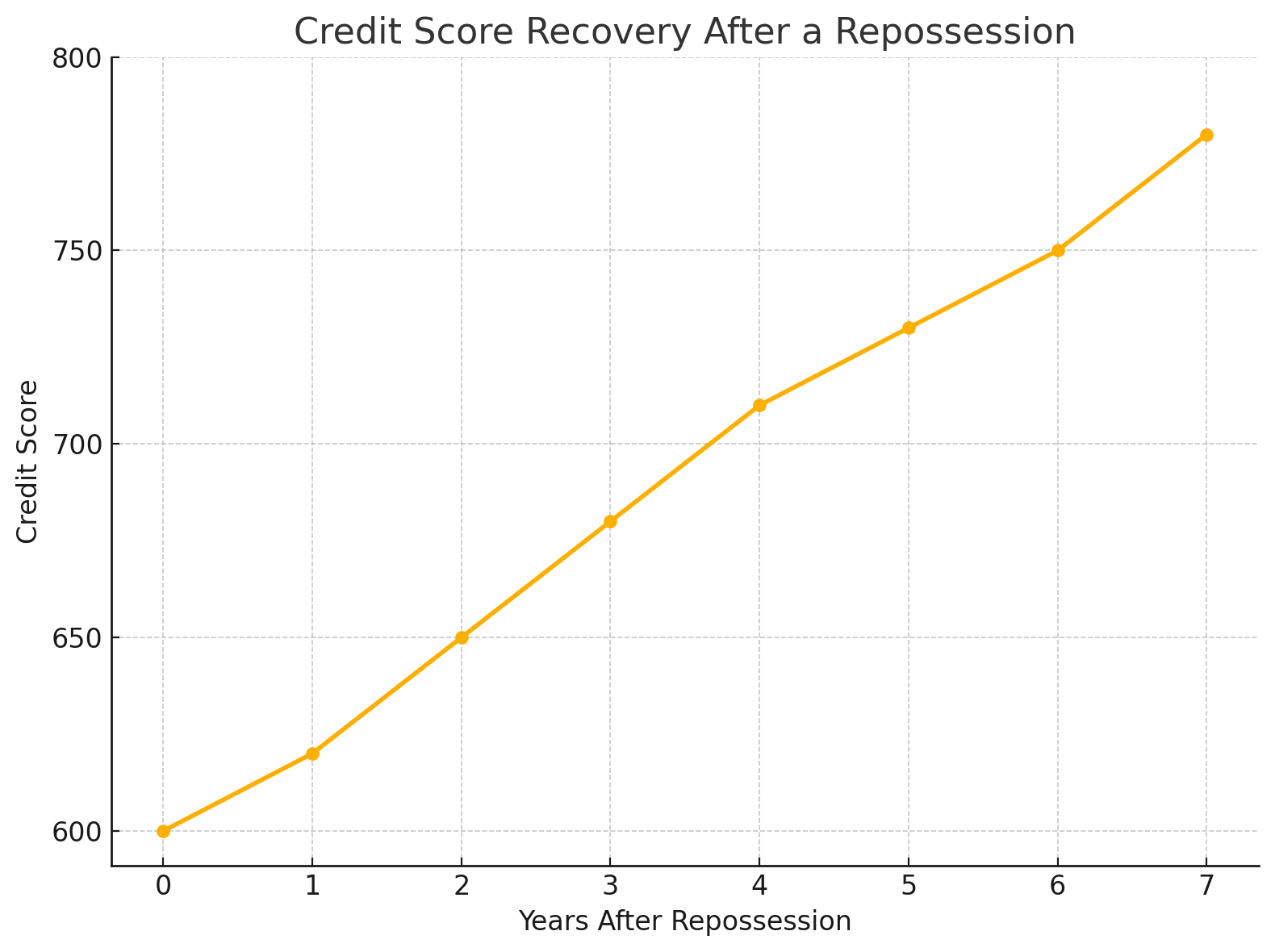

How Credit Score Recovers After a Repossession

The graph below shows the typical credit score recovery timeline after a repossession:

Steps to Rebuild Your Credit After a Repossession

While a repossession can be damaging, you can take steps to rebuild your credit over time:

1. Pay Off Outstanding Debts

If you still owe a deficiency balance after the repossession, work on settling it to avoid further collections activity.

2. Make On-Time Payments

Start making consistent, on-time payments on all other credit accounts. Payment history is crucial for rebuilding your credit score.

3. Reduce Credit Utilization

Lower your credit card balances to keep your credit utilization below 30%. This will help improve your score over time.

4. Open a Secured Credit Card

A secured credit card is a great way to rebuild credit. Use it responsibly, and it will add positive payment history to your credit report.

5. Monitor Your Credit Reports

Regularly check your credit reports for errors or signs of improvement. Use free tools like AnnualCreditReport.com or credit monitoring apps.

Frequently Asked Questions

1. How long does a voluntary repossession stay on my credit report?

A voluntary repossession stays on your credit report for 7 years from the date of the first missed payment, just like an involuntary repossession.

2. Can I get approved for a loan with a repossession on my credit?

It’s possible, but you may face higher interest rates or need to seek subprime lenders who work with borrowers with damaged credit.

3. Does a repossession affect all three credit bureaus?

Yes, repossessions are typically reported to Experian, Equifax, and TransUnion.

4. Will my credit improve after 7 years?

Yes, once the repossession falls off your report, it will no longer negatively impact your score. Your credit score should gradually improve.

5. How can I speed up credit recovery after a repossession?

Focus on responsible credit habits, like paying on time, reducing debts, and using secured credit cards to rebuild your credit profile.

Conclusion

A repossession can stay on your credit report for 7 years and significantly impact your credit score during this time. Whether voluntary or involuntary, it’s essential to take steps to minimize the damage and begin rebuilding your credit. By paying outstanding debts, disputing inaccuracies, and developing responsible credit habits, you can recover and restore your financial health.

Over time, consistent effort will help you rebuild a stronger credit profile and open doors to better financial opportunities.

Ready to Improve Your Credit?

Disputing TUIC errors is step one. Step two? Boost your score by reporting utility payments with CreditScoreIQ.

Get Started Now (Only $1 Trial) →3-bureau reporting • $1M identity insurance • Dark web monitoring