How to Remove Bankruptcy from Your Credit Report: A Complete Guide

Bankruptcy is a challenge that may accompany you during your financial life, but it is not for eternity on the credit report. If you learn how to expunge bankruptcy, you are granted a chance of manufacturing a new and better life, a good credit status will be provided to you as well as better future financial prospects. This guide will lead you through each stage and offer information and tips to help explain things in the simplest way possible.

Understanding Bankruptcy and Its Impact on Your Credit Report

Bankruptcy stays with you on your credit report for up to 10 years depending on the type of bankruptcy you have filed. Chapter 7 bankruptcy, which erases most of the forms of unsecured debt, can be reported on your credit report for up to 10 years. The case of repaying debts over time is normally completed within 7 years as stated in chapter 13. During this period a bankruptcy mark often influences your credit score and hinders your chances of getting credit, loans or even getting an apartment.

But the good news is, there are things you can do right now to change this; dispute the items in question or negotiate with the credit reporting agency. Perhaps let’s discuss them in detail.

Review Your Credit Report for Errors

The first and the most significant measure anyone can take towards attempting to delete bankruptcy out of the credit report is to demonstrate that there is something legally inaccurate with the report. It is a myth that people do not make mistakes but when they do it lengthens the lifespan of negative information.

- Get Your Free Credit Report: Obtain your credit report from each of the three major bureaus (Equifax, Experian, and TransUnion). You’re entitled to a free report annually from AnnualCreditReport.com.

- Look for Inaccuracies: Put a tick next to those fields that differ from what they should, for example: the date of bankruptcy is incorrect, there is the wrong type of bankruptcy, there is information that does not relate to the subject.

- Dispute Errors: If your details are wrong, then you have a right to challenge it with the credit bureaus. Because of this, they are required to investigate and rectify errors which may in turn lead to the wiping out of the bankruptcy.

How Long Does Bankruptcy Affect Your Credit Score?

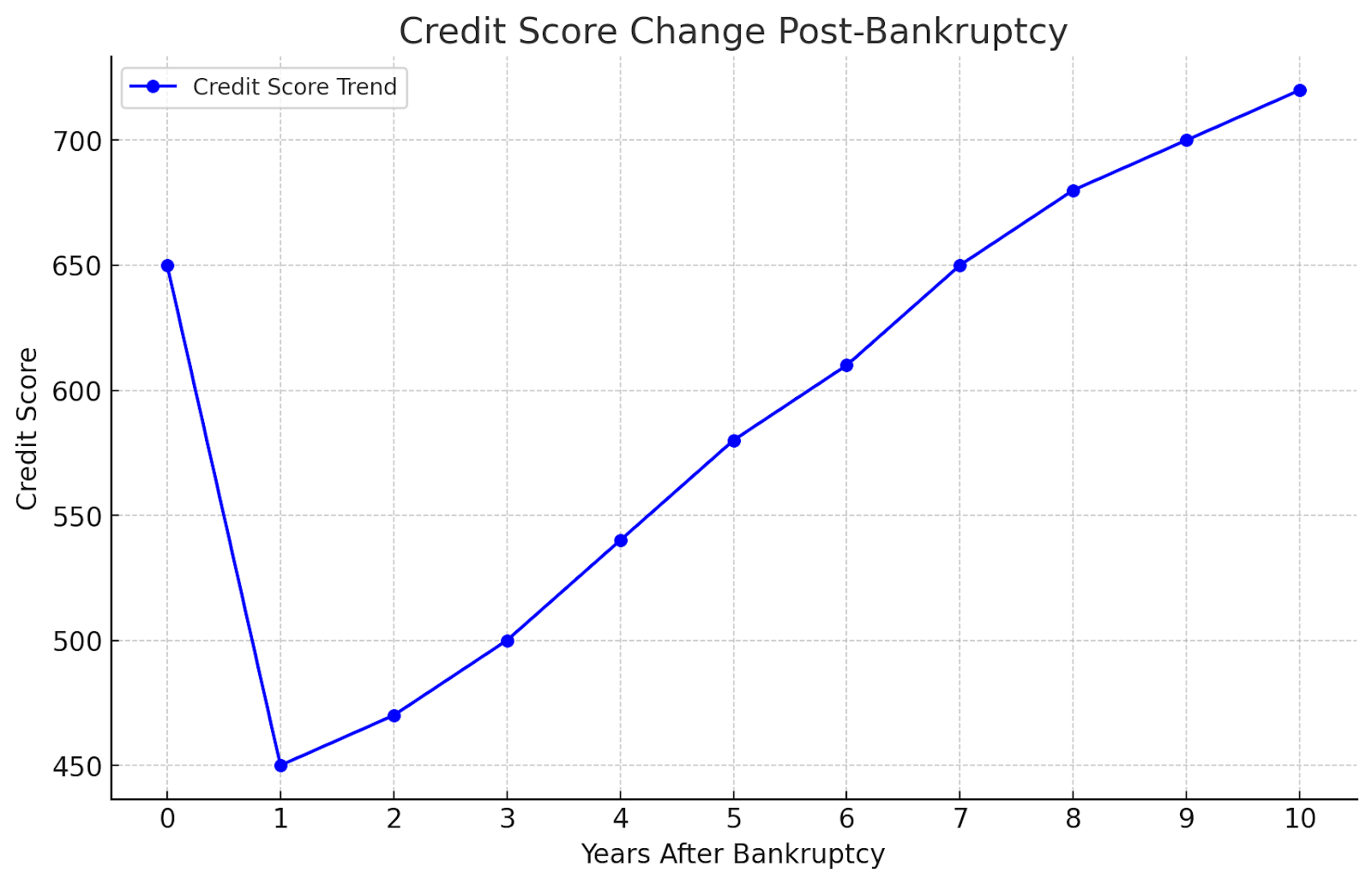

To better understand the effect of bankruptcy on your credit over time, here’s a graph showing how a typical credit score changes post-bankruptcy:

🚨 TUIC Errors + Low Credit Score?

CreditScoreIQ helps you build credit faster by reporting utility bills to all 3 bureaus—while you dispute errors.

Start Building Credit Today →

Graph showing credit score trend over 10 years after bankruptcy.

The graph illustrates how a credit score often sees a significant drop immediately after filing for bankruptcy. Over the next few years, with the right actions, such as paying bills on time, keeping credit utilization low, and disputing errors, your score can gradually increase.

Disputing the Bankruptcy Entry with the Credit Bureaus

Once you’ve checked for inaccuracies, the next step is to dispute the bankruptcy listing. Disputing can be done online or by sending a dispute letter to the credit bureaus.

Steps to Dispute:

- Gather Evidence: Collect any documents that support your case. This could include court documents or proof of identity.

- Submit Your Dispute: Contact the credit bureaus and submit your dispute online, or mail them a letter explaining the error. Include copies of supporting documents.

- Wait for Investigation: Credit bureaus typically have 30 days to respond and resolve your dispute. They will contact the court to verify information.

If the court doesn’t verify the bankruptcy or if you can prove there are errors, there’s a chance the bankruptcy will be removed.

Contact the Court

Many people don’t realize that credit bureaus verify bankruptcy information directly with the court. If you can reach out to the court and request a letter that says they do not verify bankruptcies with credit bureaus, this could work in your favor. You can provide this letter to the bureaus to help get the bankruptcy removed.

Ask for Goodwill Deletion

Another option is to contact the creditor or collection agency that was involved in your bankruptcy and ask for a goodwill deletion. This involves kindly requesting the lender to remove the negative mark from your credit report. Although creditors are not obligated to agree, many people have had success with this approach by explaining their financial struggles and how they have since turned things around.

Rebuilding Your Credit Score

Removing a bankruptcy isn’t always guaranteed, but regardless of whether the bankruptcy remains on your credit report, you can still work to rebuild your credit score. Here are some steps to take:

- Make On-Time Payments: Make sure you pay all bills on time. Payment history is a significant factor in your credit score.

- Get a Secured Credit Card: If your credit score is too low to qualify for a regular credit card, consider getting a secured card. Using it responsibly will help improve your score over time.

- Monitor Your Credit Utilization Ratio: Keep your credit utilization ratio below 30%, which means not using too much of your available credit.

Bankruptcy Timeline: When Does It Come Off?

The type of bankruptcy you filed will determine how long it stays on your credit report. Here is a quick reference table to show the differences:

| Type of Bankruptcy | Length of Time on Report |

| Chapter 7 | 10 years |

| Chapter 13 | 7 years |

If your bankruptcy has been on your report longer than the timeline shown above, you can dispute it with the credit bureaus and request its removal.

Getting Professional Help

If you’re struggling with disputing a bankruptcy on your own, it might be a good idea to seek professional help. Credit repair companies can assist with disputing errors and communicating with credit bureaus on your behalf. However, it is essential to choose a reputable service, as there are many scams in the industry.

Final Thoughts

Removing a bankruptcy from your credit report is challenging, but not impossible. By reviewing your report for inaccuracies, disputing errors, and working to rebuild your credit score, you can gradually recover and improve your financial standing. Bankruptcy may be a temporary setback, but with perseverance, you can get back on track.

Remember, even if the bankruptcy stays on your report, taking proactive steps to rebuild your credit is critical. A high credit score is achievable over time with patience and diligence.

If you have any questions or need further guidance, feel free to ask in the comments section. We’re here to help you on your path to financial freedom.

Ready to Improve Your Credit?

Disputing TUIC errors is step one. Step two? Boost your score by reporting utility payments with CreditScoreIQ.

Get Started Now (Only $1 Trial) →3-bureau reporting • $1M identity insurance • Dark web monitoring