How to Remove Settled Accounts from Your Credit Report

Settled accounts on your credit report may impact your credit score and how lenders perceive your financial health. Even though a settled account is marked as “closed,” it may still show a negative payment history or unpaid balance. If you want to improve your credit profile, removing settled accounts can make a significant difference.

In this article, we’ll discuss what a settled account is, how it affects your credit, and the steps you can take to remove it from your credit report.

What Is a Settled Account?

A settled account occurs when you pay less than the full amount owed to close a debt. For example, if you owed $5,000 and settled for $3,000, the lender writes off the remaining $2,000. While the account is marked “settled” or “paid-settled,” it can still appear as a negative item on your credit report because it wasn’t paid in full.

How Does a Settled Account Affect Your Credit?

Settled accounts can have the following effects on your credit score and report:

- Payment History Impact: If the account had missed payments or defaults, it negatively affects your credit score.

- Creditworthiness: Lenders may view a settled account as a sign that you struggled to meet your financial obligations.

- Account Status: Settled accounts remain on your credit report for up to 7 years from the original delinquency date, reducing your chances of securing credit with favorable terms.

While settled accounts are less damaging than unpaid debts, they are still seen as a negative mark.

🚨 TUIC Errors + Low Credit Score?

CreditScoreIQ helps you build credit faster by reporting utility bills to all 3 bureaus—while you dispute errors.

Start Building Credit Today →How to Remove Settled Accounts from Your Credit Report

Here are proven steps to help you remove settled accounts from your credit report:

1. Check Your Credit Report for Errors

Start by obtaining a copy of your credit report from the three major credit bureaus—Experian, Equifax, and TransUnion. You can get a free credit report annually from AnnualCreditReport.com.

What to Look For:

- Incorrect settlement amount

- Wrong payment dates

- Accounts that should no longer appear after 7 years

- Duplicate reporting

If you find errors, dispute them immediately with the credit bureau(s).

2. File a Dispute with the Credit Bureaus

If you identify inaccuracies on the settled account, file a dispute to have the errors corrected or removed. Here’s how:

- Online: Submit a dispute directly through the credit bureau’s website.

- Mail: Send a dispute letter with supporting documents to the credit bureau.

- Phone: Contact the credit bureau’s support team for guidance.

Key Tip: Always include evidence like payment receipts, settlement letters, or correspondence with the lender.

The credit bureau has 30 days to investigate and respond to your dispute. If the account cannot be verified, it will be removed.

3. Request a “Goodwill Adjustment”

A goodwill adjustment involves asking the lender to remove the settled account as a courtesy. Write a goodwill letter explaining your situation and why you’re requesting the removal. Be polite, honest, and include the following:

- Account details

- A brief explanation of why the account was settled

- How you’ve improved your financial habits since the settlement

Here’s an example:

Sample Goodwill Letter:

“Dear [Creditor’s Name],

I’m writing to request a goodwill adjustment for my account [Account Number]. I settled this account in [Month, Year], and I’ve since taken significant steps to improve my financial habits. I kindly ask you to consider removing the settled account from my credit report as a goodwill gesture. Thank you for your time and consideration._”

Lenders are not obligated to grant goodwill adjustments, but many will do so if you’ve demonstrated financial responsibility.

4. Negotiate a Pay-for-Delete Agreement

If the account is still marked “settled” but you can afford to pay the remaining balance, consider negotiating a pay-for-delete agreement with the creditor. In this agreement, you agree to pay a portion or the full amount of the remaining balance in exchange for the creditor removing the account from your credit report.

Steps to Negotiate a Pay-for-Delete Agreement:

- Contact the creditor and explain your request.

- Offer a payment amount and specify that the settled account must be removed.

- Get the agreement in writing before making any payments.

Note: Pay-for-delete agreements are not guaranteed, as not all lenders agree to remove accounts. However, it’s worth attempting.

5. Wait for the Account to Drop Off

If you can’t remove the settled account, remember that it will naturally fall off your credit report after 7 years from the date of first delinquency. As time passes, its impact on your credit score diminishes.

In the meantime, focus on improving other aspects of your credit, such as:

- Making all payments on time

- Reducing your credit utilization

- Opening a secured credit card to build positive credit history

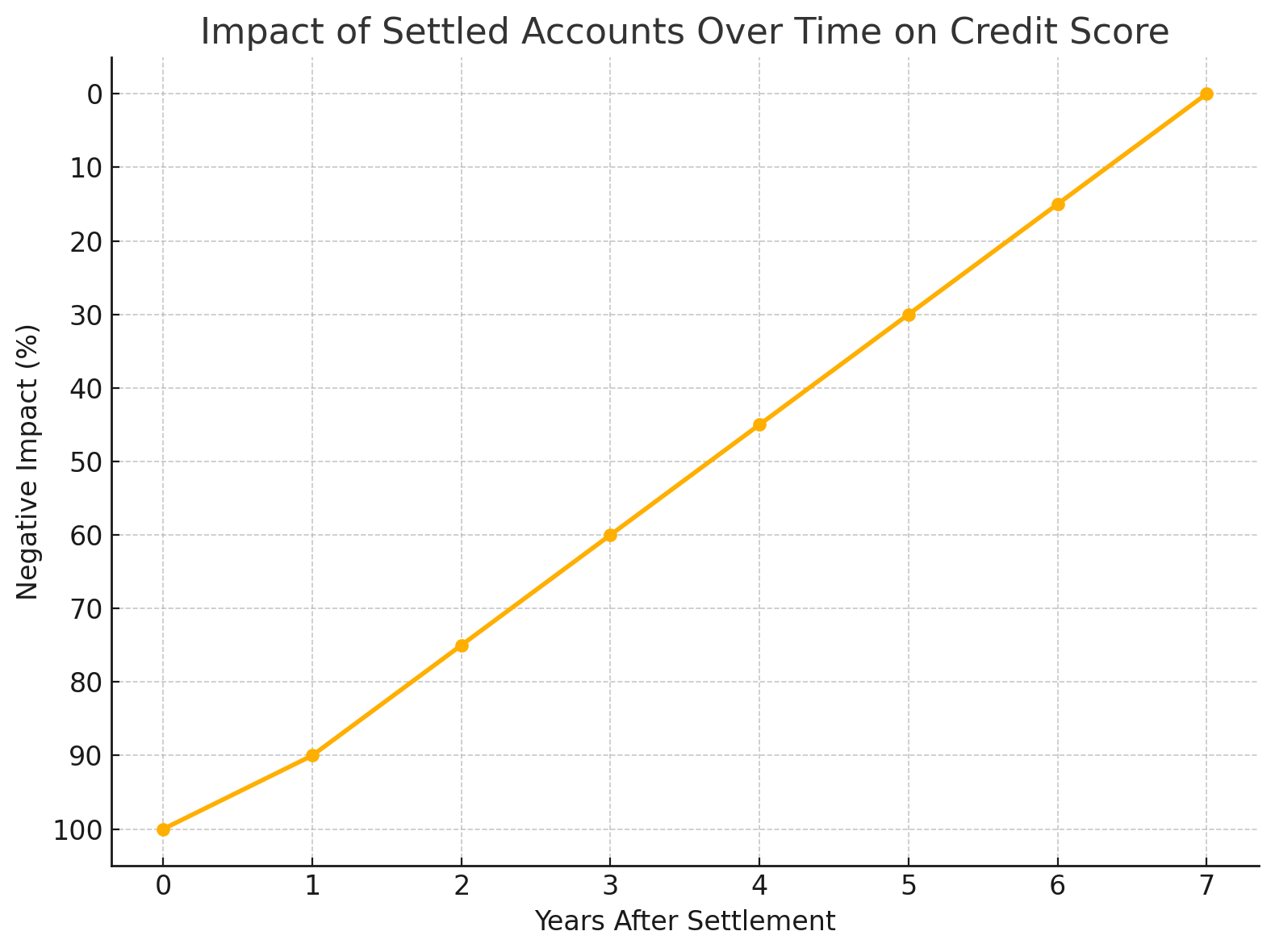

Impact of Settled Accounts Over Time on Your Credit Score

Below is a graph showing how the negative impact of settled accounts decreases as time passes:

6. Seek Help from a Credit Repair Professional

If you’re unable to remove settled accounts on your own, consider working with a reputable credit repair company. These professionals analyze your credit report, identify negative marks, and negotiate with creditors to remove or improve the accounts.

Key Tips for Choosing a Credit Repair Service:

- Avoid companies promising immediate or guaranteed results.

- Look for transparent pricing and proven success stories.

- Verify their legitimacy through reviews and accreditations.

Frequently Asked Questions

1. Can I remove a settled account from my credit report?

Yes, you can request removal through dispute errors, goodwill adjustments, or pay-for-delete agreements. However, lenders are not obligated to remove accurate information.

2. How long does a settled account stay on my credit report?

Settled accounts remain on your report for 7 years from the date of first delinquency.

3. Will removing a settled account improve my credit score?

Yes, removing a settled account can improve your credit score, especially if it was reported as a negative item.

4. What if the settled account is inaccurate?

If the settled account contains errors, you can file a dispute with the credit bureaus to have it corrected or removed.

5. Is it better to settle a debt or pay it in full?

Paying in full is better for your credit score and lender relationships. However, settling is a viable option if you cannot pay the full balance.

Conclusion

Removing settled accounts from your credit report can improve your credit score and financial outlook. Start by reviewing your credit report for errors, disputing inaccuracies, and requesting goodwill adjustments from creditors. If possible, negotiate a pay-for-delete agreement to have the account removed.

Even if you can’t remove the account immediately, focus on building positive credit habits to minimize its long-term impact. Over time, settled accounts will naturally fall off your report, and you’ll be on your way to achieving a stronger credit profile.

Ready to Improve Your Credit?

Disputing TUIC errors is step one. Step two? Boost your score by reporting utility payments with CreditScoreIQ.

Get Started Now (Only $1 Trial) →3-bureau reporting • $1M identity insurance • Dark web monitoring