When Does Chase Report to Credit Bureaus?

Despite the Chase Sapphire Reserve’s obvious value for those with decent to good credit, it’s important to know when Chase reports to credit bureaus if you are working on establishing or rebuilding credit . Like any other financial services providers, Chase reports your account details of activities that affect your credit score to the credit bureaus involved. At least, with the knowledge of their reporting frequency, you can bring your payments and other financial behaviors into your credit favor.

In the following article, we will look at when Chase Bank reports to the credit bureau, what they report to the credit bureaus, how it affects credit, and how to leverage this information.

What Does It Mean When Chase Reports to Credit Bureaus?

Reporting to credit bureaus means that Chase communicates information about your credit accounts to the three major bureaus: The three credit reporting agencies are Experian, Equifax, and TransUnion. This process includes sharing details like:

- Payment history

- Current balance

- Credit utilization

- Account age

- Account status (open or closed)

- Credit limit

This information is used to determine your credit score. Chase’s reporting impacts your overall financial well-being because credit scores determine your capability of obtaining loans, credit cards, mortgages and rental agreements.

When Exactly Does Chase Report?

Truth be told, Chase usually updates credit bureaus at the close of your billing cycle not the payment due date. This means the information reported to credit bureaus is the status of your account as stated on the closing date of the statement. After that, if Chase has submitted the data, it can take between about 3 to 5 business days for the bureau to report it on your credit file.

🚨 TUIC Errors + Low Credit Score?

CreditScoreIQ helps you build credit faster by reporting utility bills to all 3 bureaus—while you dispute errors.

Start Building Credit Today →For example:

- Billing cycle closes: November 15

- Report date: November 16 or 17

- Data visible on credit report: Around November 20

While Chase’s reporting schedule is consistent, slight delays may occur due to holidays or processing times.

How Chase Reporting Affects Your Credit

Another reason by which the timing of Chase’s reporting hurts your credit score in several ways. Here are the key factors:

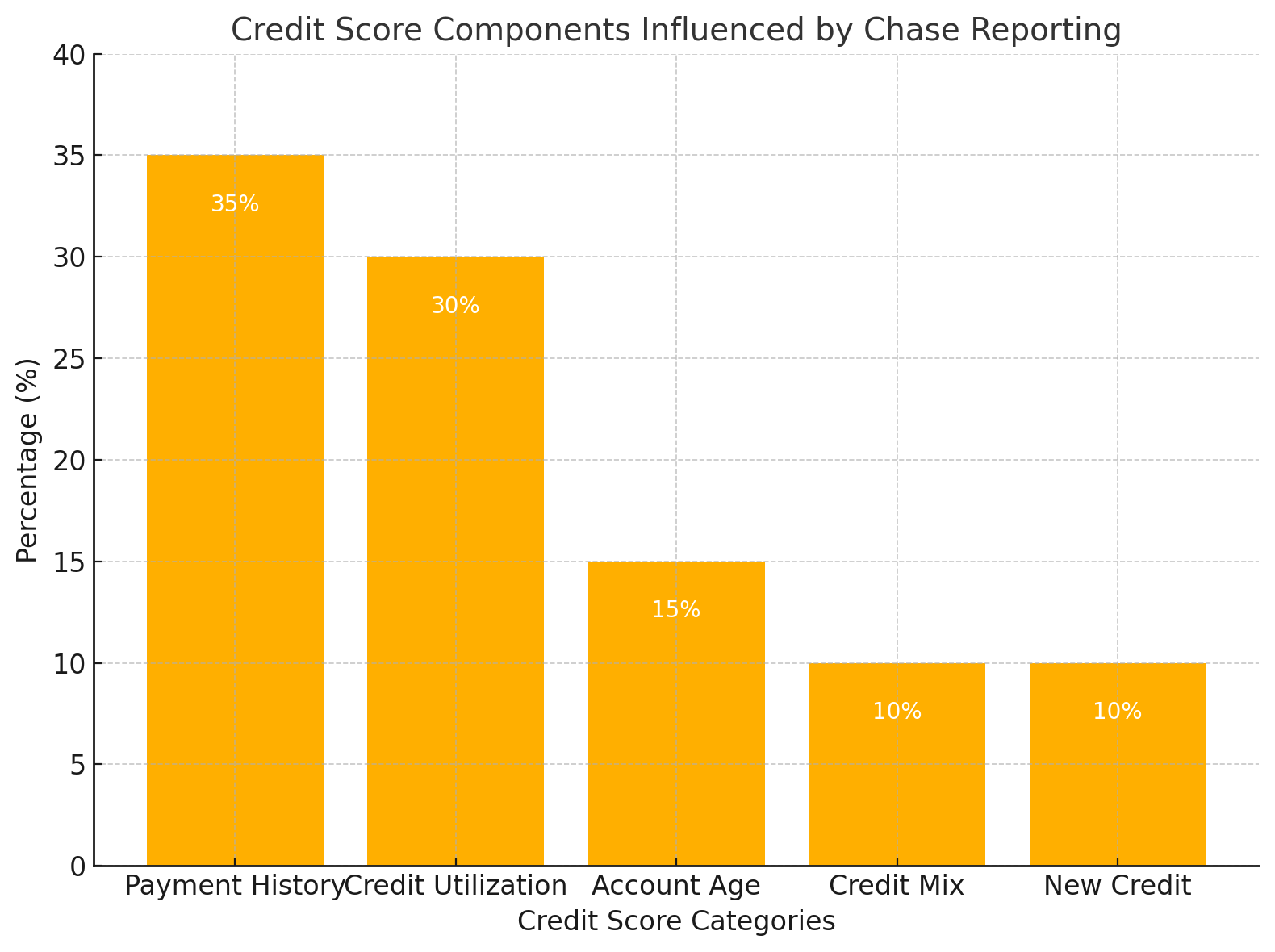

1. Payment History

A record you have made as a paymaster and paymaker stands as the most influential in composing FICO score, contributing to 35 percent of the total score. Chase informs you whether you made the payment or missed the payment. Paying on time means you are good on your credit report thus increasing your score with time.

2. Credit Utilization

Chase reports your current balance relative to your credit limit, which is known as your credit utilization ratio. A ratio under 30% is ideal for a healthy credit score. For example, if your credit limit is $10,000, aim to keep your reported balance below $3,000.

3. Account Age

The length of time your accounts have been active also affects your credit score. Chase reports the opening date of your accounts, contributing to your credit age. Keeping older accounts open helps improve this factor.

4. Credit Mix

Chase’s credit cards contribute to your credit mix, which accounts for 10% of your score. Having a variety of credit types—like credit cards, auto loans, and mortgages—demonstrates financial responsibility.

5. Derogatory Marks

If you miss payments, default, or close an account in bad standing, Chase reports these negative events, which can significantly lower your credit score.

Key Factors in Chase Credit Reporting

| Factor | Details |

| Reporting Frequency | Monthly |

| Reporting Timing | After the billing cycle ends |

| Impacted Score Areas | Payment history, utilization, account age |

| Delay Before Visible | 3–5 business days on credit reports |

| Best Practices | Pay balances before the billing cycle ends |

Credit Score Breakdown Impacted by Reporting

Here’s a graphical representation of how Chase’s reporting influences different components of your credit score:

Why Timing Matters for Your Credit Strategy

Knowing when Chase reports to credit bureaus allows you to control what data gets reported. By managing your payment schedule and balances strategically, you can ensure that only favorable information impacts your credit score. Below are a few tips to maximize this knowledge:

1. Pay Balances Before the Billing Cycle Ends

If you want a lower balance reported, make an early payment before your statement closing date. For example, if your cycle ends on the 15th, ensure your payment clears by the 14th.

2. Avoid Late Payments

One late payment can severely damage your credit score. Set up auto-pay or reminders to ensure timely payments.

3. Monitor Your Credit Reports

Regularly check your credit reports from Experian, Equifax, and TransUnion to verify that Chase has reported accurate data. Dispute any errors promptly.

4. Keep Credit Utilization Low

Aim to keep your utilization ratio below 30%, but for the best results, try maintaining it under 10%. High utilization can lower your credit score even if you pay in full after the billing cycle.

Frequently Asked Questions

1. How often does Chase report to credit bureaus?

Chase reports account activity to credit bureaus once a month, usually after the statement closing date.

2. What information does Chase report?

Chase reports payment history, current balances, credit limits, account age, and account status.

3. How long does it take for the information to appear on my credit report?

Once Chase submits the data, it typically appears on your credit report within 3–5 business days.

4. Can I request Chase to report earlier?

No, reporting schedules are standardized and cannot be customized upon request.

5. What happens if Chase reports incorrect information?

You can file a dispute with the credit bureau to correct any inaccuracies. Alternatively, contact Chase customer service to resolve the issue.

How to Check When Chase Reports to Credit Bureaus

To confirm the exact reporting timeline for your account, follow these steps:

- Review Your Statement Dates

Check the closing date on your credit card statement. Chase reports shortly after this date. - Monitor Your Credit Report

Look for recent updates to your credit report from Chase. Free credit report tools like Credit Karma or AnnualCreditReport.com can help. - Contact Customer Service

Call Chase customer service for clarification about their reporting schedule for your specific account.

Best Practices to Optimize Your Credit Score with Chase

Taking proactive steps can help you use Chase’s reporting to your advantage:

1. Early Payments

Pay off balances or reduce them significantly before the billing cycle closes to show low credit utilization on your credit report.

2. Avoid High Balances

Even if you pay off your credit card in full each month, high balances reported at the cycle’s end can hurt your score. Spend wisely to maintain a low ratio.

3. Keep Old Accounts Open

Avoid closing older accounts, as they contribute to your credit age, which impacts 15% of your score.

4. Track Payment Dates

Set reminders to ensure you never miss a payment. Automating payments is a reliable option.

Conclusion

Understanding when Chase reports to credit bureaus is an essential part of managing your credit score. Typically, Chase reports shortly after the end of your billing cycle, and this data significantly impacts your payment history, credit utilization, and overall financial health. By paying balances early, avoiding late payments, and monitoring your credit reports regularly, you can ensure Chase’s reporting works in your favor.

Use this knowledge strategically to improve your creditworthiness and achieve your financial goals. Whether you’re aiming to secure a mortgage, qualify for a new credit card, or simply maintain excellent credit, being proactive with Chase’s reporting schedule can make all the difference.

Ready to Improve Your Credit?

Disputing TUIC errors is step one. Step two? Boost your score by reporting utility payments with CreditScoreIQ.

Get Started Now (Only $1 Trial) →3-bureau reporting • $1M identity insurance • Dark web monitoring